Front Spread w/Puts

AKA RATIO VERTICAL SPREAD

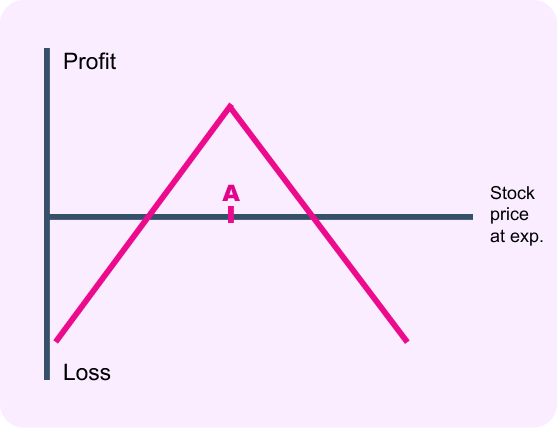

Buying the put gives you the right to sell stock at strike price B. Selling the two puts gives you the obligation to buy stock at strike price A if the options are assigned.

The strategy

Buying the put gives you the right to sell stock at strike price B. Selling the two puts gives you the obligation to buy stock at strike price A if the options are assigned.

This strategy enables you to purchase a put that is at-the-money or slightly out-of-the-money without paying full price. The goal is to obtain the put with strike B for a credit or a very small debit by selling the two puts with strike A.

Ideally, you want a slight dip in stock price to strike A. But watch out. Although one of the puts you sold is “covered” by the put you buy with strike B, the second put you sold is “uncovered,” exposing you to significant downside risk.

If the stock goes too low, you’ll be in for a world of hurt. So beware of any abnormal moves in stock price and have a stop-loss plan in place.

Options guys tips

You’re slightly bearish. You want the stock to go down to strike A and then stop.